The $300M Round That Redrew the Defense Startup Map

On June 2, 2026, Mach Industries announced a $300 million Series C led by Infinite Capital and Ribbit Capital, with participation from existing investors Bedrock Capital, Sequoia Capital, and Khosla Ventures. The round values the Huntington Beach, California company at $1.8 billion — up from $470 million just twelve months earlier, a quadrupling that would be remarkable for any startup but is especially striking for a hardware-intensive defense manufacturer only three years into its existence.

The company was founded in 2023 by Ethan Thornton, who was 22 at the time, making him one of the youngest founders ever to helm a defense unicorn. That age point is not incidental: Thornton’s biography is central to how Mach Industries has pitched itself — as a generation of builders willing to re-examine industrial constraints that incumbents like Raytheon or Northrop Grumman treat as fixed. TechCrunch reported that Thornton initially set out to raise $200 million and ended up oversubscribed: “We went out to raise 200 [million dollars] and we were extremely oversubscribed at 200.”

The oversubscription is a signal that institutional capital has moved past asking whether defense tech is a legitimate venture category and toward competing to own the winners early.

Five Systems, One Thesis: Speed Beats Specification

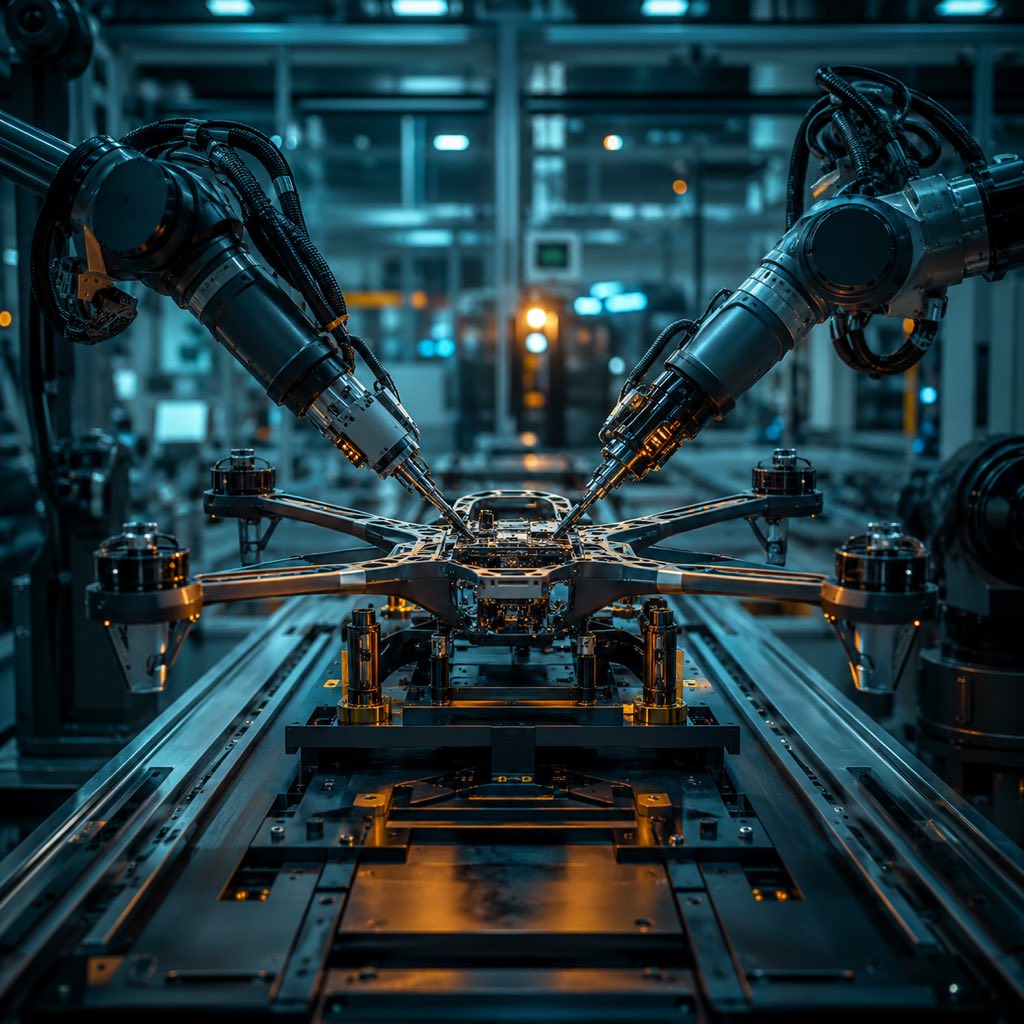

Where many defense tech startups have pivoted toward software — AI-powered ISR, logistics optimization, command-and-control dashboards — Mach Industries has held firm on the hardest part: building the physical systems themselves, and doing so faster and cheaper than the primes.

The company currently operates five active vehicle programs:

- Viper — a jet-powered vertical take-off one-way strike vehicle

- Glide — a high-altitude strike glider designed for weapons launching

- Stratos — an airborne surveillance platform

- Dart — a low-cost counter-drone interceptor

- Pike — a long-range strike munition intended for large-scale deployment

A sixth program — a runway-independent Navy strike aircraft — was announced alongside the Series C. According to the press release, Mach expects to begin production on at least three of these systems during 2026, an unusually rapid transition from development to production for defense hardware.

The speed claim is backed by a concrete precedent. Mach Industries built a functioning jet engine in eight months — a timeline that traditionally takes four years at established aerospace firms. That achievement, rather than any government contract award, became the company’s primary recruiting and investor pitch.

Mach Industries also recently acquired Exquadrum, a solid rocket motor startup, for $50 million. The acquired entity has been rebranded as Mach Energetics and will serve dual purposes: internal propulsion for Mach’s own vehicles and external commercial rocket motor sales. The move is a direct expression of the vertical integration logic — controlling propulsion removes a key dependency and adds a revenue line.

Advertisement

The Manufacturing Infrastructure Bet

The real thesis at Mach Industries is not about any single weapon system. It is about manufacturing infrastructure. The company currently operates a 115,000-square-foot facility in Huntington Beach and is planning four additional production facilities by the end of 2026. The workforce stands at approximately 350 employees.

Infinite Capital founder Nathan Doctor summarized the investor view: the company has demonstrated “unprecedented speed to flight, production trajectory” — a phrase that maps directly to the Pentagon’s persistent frustration with its traditional procurement base. The Department of Defense has spent two decades watching its prime contractors deliver systems late, over budget, and in quantities below requirement. Mach’s pitch is that a startup operating outside that culture can produce autonomous strike systems at the pace and volume that modern conflict demands.

The company lists the U.S. Army, Air Force, and Special Operations Command (SOCOM) as customers, alongside allied governments — though specific contract values have not been disclosed, as confirmed in Defense Daily’s coverage of the round. What matters structurally is that these are not pilot agreements or research contracts: they are relationships with the operational procurement community, the offices that actually buy weapons at scale.

What Investors and Founders Should Do About This Signal

1. Treat Vertical Integration as a Moat, Not a Cost Center

The conventional startup wisdom — outsource everything, focus on IP, stay asset-light — inverts in defense hardware. Mach’s acquisition of Exquadrum illustrates the logic: by owning propulsion, the company gains cost control, production speed, and a barrier to replication that a software-only competitor cannot build. Founders entering the defense manufacturing space should map their bill-of-materials and identify the two or three components where supplier dependency creates the most schedule and margin risk. Those are acquisition targets, not procurement relationships.

2. Benchmark Speed Metrics Explicitly in Your Investor Materials

Mach Industries built a jet engine in eight months against a four-year industry baseline. That comparative figure — not “we’re faster than incumbents” in abstract — is what closed a $300M oversubscribed round. Defense tech investors increasingly use “time to flight” or “time to first article” as primary due-diligence metrics alongside burn rate and team quality. Founders should document their development timelines against named industry benchmarks and lead with those numbers. If you cannot produce the comparison, investors will construct their own, usually unfavorably.

3. Design for Production Volume from Day One, Not as a Phase Two Problem

The transition from prototype to production is where most defense hardware startups stall. They optimize for getting a system to fly or function, then discover that scaling to 1,000 units per year requires a completely different organizational and supply-chain architecture. Mach’s planning of four production facilities by end-2026 — while still in development — reflects a manufacturing-first mentality. Series A and B founders building physical defense systems should bring a production engineer onto the core team before the first demo, not after the first contract.

4. Position US-Based Manufacturing as a Strategic Asset, Not a Cost Disadvantage

The political environment in 2026 — reshoring mandates, Buy American requirements, security constraints on supply chains — has turned US-based manufacturing from a cost burden into a competitive moat for defense contractors. Mach’s Huntington Beach facilities and its planned expansion are not just operational choices; they are regulatory positioning. Startups building defense hardware offshore or with significant international supplier exposure face increasing friction in government procurement. The Series C investors are partly underwriting that domestic footprint.

Where This Fits in 2026’s Defense Tech Ecosystem

Mach Industries’ $1.8B valuation and oversubscribed Series C arrive at a specific moment in the defense tech funding cycle. The Ukraine conflict and Taiwan Strait tensions have created sustained political support for accelerating autonomous weapons procurement outside the traditional primes, and venture firms that were hesitant to touch defense hardware pre-2022 are now competing for allocation.

What distinguishes this round is not the amount — $300M is becoming common at this stage — but the composition. Ribbit Capital is a fintech-origin fund with no prior defense portfolio. Sequoia and Khosla are general-purpose technology investors. That crossover from pure defense-tech specialists to generalist top-tier VCs is the clearest signal that Mach Industries has crossed from “defense niche” into “credible technology unicorn” territory.

The company’s next inflection will be execution-dependent: whether it can actually begin serial production on three systems in 2026, whether the Mach Energetics commercial rocket motor business develops a standalone revenue profile, and whether the four planned facilities can be stood up on schedule. A $1.8B valuation on a company with no disclosed revenue requires a production ramp that converts investor conviction into delivered units. That is the test every investor in this round is watching.

Frequently Asked Questions

What does Mach Industries actually make?

Mach Industries develops autonomous unmanned defense systems, including Viper (a jet-powered vertical take-off strike vehicle), Glide (a high-altitude strike glider), Stratos (a surveillance platform), Dart (a counter-drone interceptor), and Pike (a long-range strike munition). The company also recently acquired solid rocket motor maker Exquadrum, rebranded as Mach Energetics, enabling in-house propulsion manufacturing.

Why did Mach Industries’ valuation quadruple in one year?

The jump from $470 million to $1.8 billion reflects both broader defense tech investor enthusiasm following geopolitical tensions and Mach’s specific execution: building a functional jet engine in eight months versus the industry-standard four years, securing Army, Air Force, and SOCOM as customers, and demonstrating a credible path to serial production. The $300M round was oversubscribed, with founder Ethan Thornton noting the company originally targeted only $200 million.

Who are Mach Industries’ investors and what do they signal?

Lead investors Infinite Capital and Ribbit Capital are joined by Bedrock Capital, Sequoia Capital, and Khosla Ventures. The participation of Ribbit (fintech-origin) and generalist tier-one VCs like Sequoia signals that Mach has crossed from a niche defense bet into mainstream technology portfolio territory — a validation that defense hardware startups can command valuations and investor profiles previously reserved for software unicorns.

Sources & Further Reading

- Mach Industries Raises $300 Million in Series C Funding — PR Newswire

- Defense Tech Darling Mach Industries Hits $1.8B Valuation, a 4x Jump in a Year — TechCrunch

- Mach Industries Raises $300 Million Series C at $1.8 Billion Valuation — Pulse2

- Mach Industries Raises $300 Million to Advance Systems Production — Defense Daily

🔗 Related Intelligence

Defense Tech’s Venture Gold Rush: From Ethical Taboo to $49 Billion Sector

Hermeus Hits $1B Valuation: The Startup Building Mach 5 Unmanned Aircraft

Defense Tech’s Dual-Use Surge: How Helsing’s €12B Valuation and 70% Scaleup Capital Are Rewriting the VC Playbook

Lockheed Martin Ventures Doubles to $1B: Largest Defense CVC Expansion Since 2007 Targets National-Security Startups