A Landmark Round at a Critical Inflection Point

On June 3, 2026, Oxford Quantum Circuits (OQC) announced the close of its Series C round at £260 million — equivalent to roughly $350 million. The round was oversubscribed, led by Bullhound Capital (with partner Per Roman joining OQC’s board), and backed by a broad syndicate that included the British Business Bank, Rokos Capital Management, Chevron Technology Ventures, Fulcrum Asset Management, Pentland Ventures, Magdalen College Oxford, Alpha Edison, COFIDES, and returning investors Oxford Science Enterprises, SBI, and the University of Tokyo Edge Capital Partners. J.P. Morgan served as placement agent.

No comparable private quantum funding event has occurred in Europe before this. The round represents a strong endorsement of the UK’s position in the global quantum race, and it arrived during the Prime Minister’s London Tech Week address — at which UK Chancellor Rachel Reeves simultaneously announced a £2 billion government commitment to support quantum companies reaching commercial scale.

CEO Gerald Mullally put the moment succinctly: “This marks a shift in quantum computing from long-term promise to near-term delivery.” That phrase is not marketing. It is a structural description of where OQC sits in the quantum stack: not a research lab seeking proof-of-concept grants, but a company deploying revenue-generating quantum infrastructure in partner data centres across three continents.

What Makes OQC Different: The Coaxmon Architecture

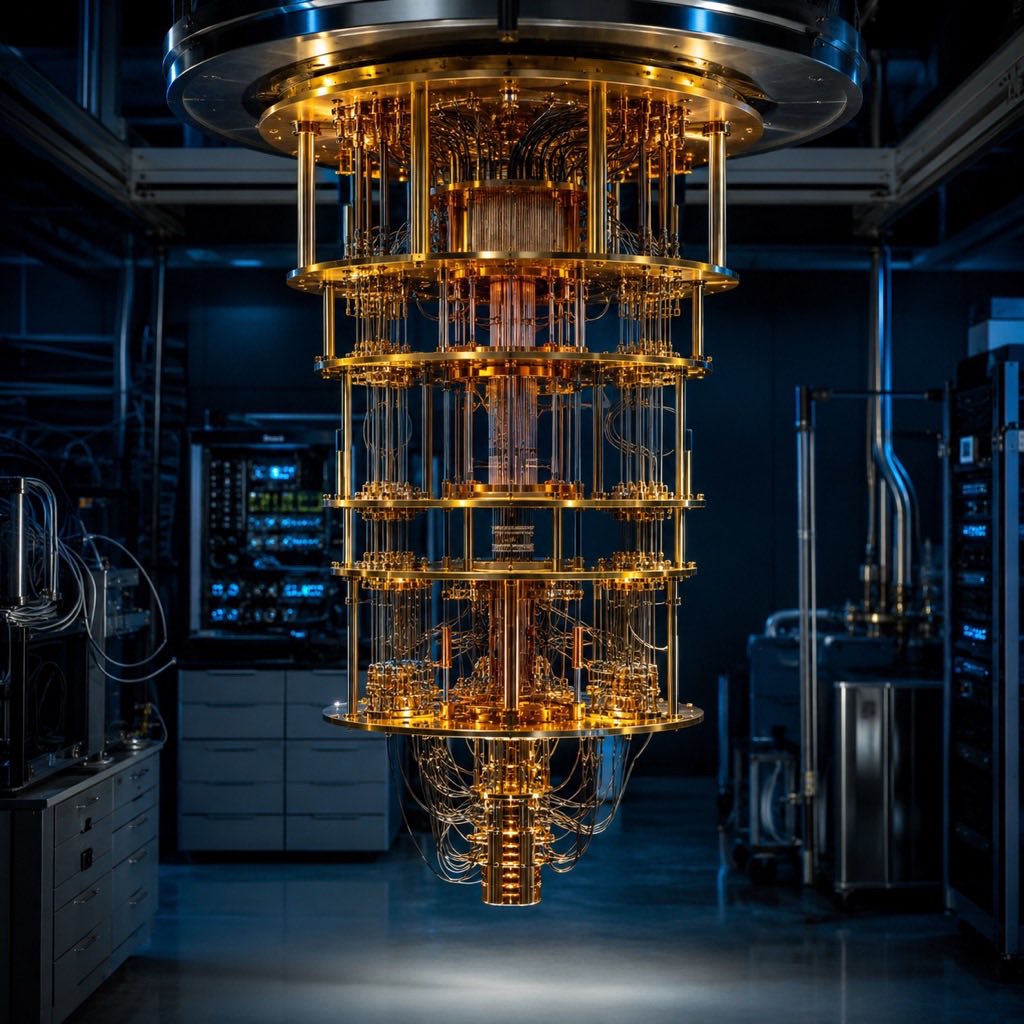

OQC was founded in 2017 by Dr. Peter Leek as a spinout from the University of Oxford’s Department of Physics. Its core differentiation is the Coaxmon — a three-dimensional superconducting qubit architecture that places qubit components on opposite sides of a substrate, simplifying the wiring problem that has historically made scaling superconducting quantum processors extremely difficult.

Unlike approaches that pack all components on a flat 2D plane, the Coaxmon’s geometry separates control lines from qubit planes, reducing interference and improving coherence times — the window of time during which qubits retain quantum states long enough to be useful. A February 2026 preprint from OQC’s engineering team demonstrated wafer-scale packaging supporting over 500 superconducting qubits on a single 3-inch die, with a median T₁ (energy relaxation time) of 97 microseconds. That is a significant materials and fabrication milestone.

The current commercial system runs on 32 qubits with two-qubit gate fidelity benchmarked at 99.8% and gate speeds of 25 nanoseconds. These are the operational metrics that enterprise customers — particularly in financial modelling, defence cryptography, and molecular simulation — care about: fidelity and speed, not just raw qubit count.

OQC’s published technology roadmap escalates systematically:

- GENESIS — 16 logical qubits, targeted for 2026

- TITAN — 200 logical qubits, targeted for 2028

- ATHENA — 5,000 logical qubits, targeted for 2031

- ATLAS — 50,000 logical qubits, targeted for 2034

The gap between 32 physical qubits today and 50,000 logical qubits by 2034 involves error correction layers that are still being worked out across the entire field. But OQC is one of a handful of companies with both the hardware credibility and the commercial infrastructure to make that roadmap trajectory plausible.

Advertisement

Quantum-as-a-Service: The Business Model That Changes Everything

The most commercially important aspect of OQC’s operation is not its hardware — it is its deployment model. As CEO Mullally explains: “Customers buy time on our quantum computer, rather than buying a quantum computer.”

This Quantum-as-a-Service (QaaS) model mirrors what cloud computing did for enterprise IT in the 2010s: it eliminates the need for customers to invest in cryogenic infrastructure, specialist personnel, or hardware refresh cycles. Instead, enterprise clients access quantum processors via partner data centres — currently including Equinix and Digital Realty facilities in London, Tokyo, and New York, plus the CESGA supercomputing centre in Spain, with additional locations pending announcement.

The global quantum computing market is projected to grow at approximately 22% CAGR through 2033, beginning from a 2026 base of roughly $1.9 billion. Cloud-based quantum access now accounts for approximately 48% of enterprise quantum deployments, according to market research — a figure that validates OQC’s infrastructure-first strategy. Financial services alone account for over 46% of commercial quantum use cases, with pharmaceutical research and manufacturing optimization absorbing much of the remainder.

The November 2025 partnership with Fraunhofer EMFT — Europe’s leading semiconductor fabrication research institute — further strengthens OQC’s manufacturing capability, adding an industrial-scale quantum fabrication partner to its supply chain at a moment when scaling from 32 to hundreds of physical qubits requires new packaging and integration techniques.

What Enterprise Teams Should Do

The £260M round is a market signal, not just a company milestone. For technology and strategy leaders across sectors, it compresses the timeline on quantum planning decisions that many organizations have been deferring.

1. Map your quantum computing readiness now

Most organizations have not systematically catalogued which of their computational workloads are candidates for quantum acceleration. That audit needs to happen now — before quantum access becomes competitively priced and before your competitors have already identified their use cases. Prioritize: optimization problems with large combinatorial search spaces (logistics, supply chain, portfolio construction), simulation tasks (molecular dynamics, materials science, risk modelling), and cryptographic workloads that will eventually require quantum-resistant algorithms. The audit does not require quantum expertise; it requires cataloguing what currently runs on classical HPC or takes unreasonably long to solve.

2. Explore cloud-based quantum access before committing hardware

OQC’s QaaS model — and analogous offerings from IBM Quantum, Amazon Braket, and Azure Quantum — means there is no hardware investment required to start experimenting. Your teams can access 32-qubit superconducting systems today through existing data centre agreements. The appropriate entry point is a small, bounded proof-of-concept: take one hard optimization problem, run it on a quantum backend alongside a classical baseline, and measure the performance gap. The results will either confirm that quantum is not yet ready for your workload (a useful finding that saves budget) or reveal a genuine speedup worth pursuing. Either outcome is more valuable than continued deferral.

3. Identify use cases where quantum beats classical today

Despite the excitement, quantum advantage over classical computers today is narrow and specific. The areas where near-term quantum systems (50-200 qubits with error correction) are expected to deliver practical speedups in the 2026-2028 window include: variational quantum eigensolvers for molecular simulation, quantum approximate optimization algorithms (QAOA) for portfolio optimization, and quantum key distribution (QKD) for cryptographic infrastructure. If your organization operates in financial services, pharmaceuticals, or government security, these use cases deserve a dedicated quantum task force now. For most other sectors, the right posture is structured monitoring — not waiting passively, but tracking OQC’s TITAN milestone (200 logical qubits by 2028) as the inflection point that may enable broader commercial advantage.

Why This Round Changes the Quantum Timeline

The £260M Series C does something no press release can fully capture: it removes the “if” from the quantum commercial question and replaces it with “when.” The combination of an oversubscribed round at this scale, a government matching commitment of £2 billion, and a deployment footprint already spanning four countries tells a coherent story.

For startups and scale-ups building adjacent to quantum (post-quantum cryptography vendors, quantum software layer companies, data centre operators who will need to host these systems), the OQC round accelerates the competitive timeline. For enterprises in finance, defence, and advanced manufacturing, it establishes 2028 — when OQC’s TITAN system is expected to hit 200 logical qubits — as a credible planning horizon for quantum advantage in constrained problem domains.

The round also matters geopolitically. Europe has watched the US (through IBM, Google, IonQ, and Quantinuum) and to a lesser extent China define the quantum computing agenda for the past decade. OQC’s £260M close, anchored in Oxford and backed by a consortium that spans Singapore-based investors (Adaptive Capital Partners), Japanese institutions (University of Tokyo Edge Capital Partners), and US-based funds, signals that European quantum infrastructure is now genuinely competitive on a global basis — not just in research output, but in commercial deployment.

Dr. Peter Leek’s founding vision — “engineered systems that scale as simply as possible” — was always a commercial thesis, not just a physics ambition. The £260M Series C is the market’s confirmation that the engineering is working.

Frequently Asked Questions

What is the Coaxmon architecture that OQC uses?

Answer: The Coaxmon is a three-dimensional superconducting qubit design developed at the University of Oxford. Unlike conventional 2D superconducting qubit layouts, the Coaxmon places qubit components on opposite sides of a substrate — separating control wiring from qubit elements. This geometry reduces electromagnetic interference, improves qubit coherence times, and makes scaling to higher qubit counts more tractable from an engineering standpoint. OQC’s current commercial system runs 32 physical qubits using this architecture, with a roadmap targeting 200 logical qubits by 2028.

Why is the £260M round described as Europe’s largest private quantum funding round?

Answer: The designation refers specifically to private (venture and institutional) funding rounds for European-headquartered quantum computing companies, excluding government grants and public procurement contracts. Prior to OQC’s Series C (closed June 3, 2026), no European quantum company had raised a comparable sum in a single private funding event. The round was also oversubscribed, indicating investor demand exceeded the £260M target — a strong market signal in a sector that has historically struggled to attract generalist institutional capital at this scale.

How do enterprise customers access OQC’s quantum systems today?

Answer: OQC operates a Quantum-as-a-Service (QaaS) model: customers purchase computing time on OQC’s quantum processors rather than purchasing hardware. Systems are deployed in partner data centres — currently Equinix and Digital Realty facilities in London, Tokyo, and New York, plus the CESGA supercomputing centre in Spain — meaning access is available through standard data centre commercial agreements. Enterprise clients in financial services, defence, and security are OQC’s primary target customers. Access typically begins with a proof-of-concept engagement scoped to a specific optimization or simulation workload.

Sources & Further Reading

- Further Reading

- OQC Series C Announcement — OQC Newsroom

- Oxford Quantum Circuits Raises £260M in Oversubscribed Series C — Sifted

- OQC Raises £260 Million in Series C — The Quantum Insider

- British Business Bank Commits £100M to Oxford Quantum Circuits — British Business Bank

- Oxford Quantum Circuits Unveils Roadmap for 50,000 Logical Qubits — Tech Journal UK

- Quantum Computing Market Size & Share Report 2026-2033 — Grand View Research

- OQC Lands “Coming-of-Age” £260M Funding Round — Tech.eu

🔗 Related Intelligence

IBM Quantum Cloud at 10: From Lab Curiosity to Enterprise-Grade Infrastructure Practice

Orbital Industries’ $50M Series B: AI-Designed Materials Aim at the Data Center Build-Out

Q1 2026 Hits $297B: How Mega-Rounds Ate the Seed Stage and What Founders Should Do

Beyond Software: Deep Tech Hardware Startups in Quantum, Photonic